Deep Dive: L'Occitane (973.HK)

Big potential from Sol de Janeiro – likely beating market expectation and intrinsic value not fully baked into valuation

Disclaimer: L’Occitane has been undergoing a privatization process, and the latest update is that the company has met the privatization criteria, receiving over 90% of the votes in favor from minority shareholders. As a result, the firm will soon be privatized at a price of HK$34 per share, meaning the stock will be off the market.

Despite this, I believe the analysis below remains valuable. The report was written in early April, before the privatization, and provides insights into the business fundamentals and my assessment of its intrinsic value. The analysis might help explain part of the reasons why the company pursued privatization, the value they (company management) saw in the business, and why I believe it is a “good deal” for the buyers (the company and Blackstone). Although the stock can no longer be purchased, the research itself could be valuable for analyzing similar businesses in the future.

Disclaimer: This research is for informational purposes only. This is NOT a recommendation to buy or sell securities discussed. Please do your ownwork before investing your money.

Note: L’Occitane’s fiscal year ends on March 31st. For the purposes of this report, I refer to FY2023 as 2022, which was the most recent fiscal year available at the time of writing. This fiscal year covers the period from April 1, 2022, to March 31, 2023.

Big potential from Sol de Janeiro – likely beating market expectation and intrinsic value not fully baked into current valuation; BUY

Date: Apr 08, 2024; Stock price: HK$29.5; Target price: HK39.5 (34% upside)

L’Occitane Inc. is a global collection of premium beauty and personal care brands, including L’Occitane en Provence, Sol de Janeiro (SDJ), Elemis, and a few other smaller brands. Upon delving deeper into the company, I’ve grown fond of the recently acquired SDJ brand, and believe it can contribute significantly to the Group’s valuation. I valued SDJ alone at €3.6bn (for L’Occitane’s share), or 71% of the entire company’s valuation - this highlights a discrepancy as the market instead attributes the bulk of the company’s value to its main brand, L’Occitane en Provence. A possible explanation is that due to the relatively smaller size and early stage of development of SDJ, the market has not fully realized its intrinsic value - providing us an opportunity to buy the stock at this moment.

Investment thesis

Short-term revenue beat: the street is expecting SDJ to deliver 40-60% revenue growth in 2024; however, I think there is a high chance that SDJ will exceed the higher end of the projections by expanding its presence in the Ulta channel and increasing its footprint in international markets

Undervaluation of SDJ: I feel the market currently views SDJ as a brand with high potential yet ranks it as secondary to L’Occitane en Provence, the flagship brand, thus not respecting it with enough valuation. My model suggests that SDJ will surpass L’Occitane en Provence’s revenue in 2025, and surpass the latter’s EBIT in 2024. I value SDJ (L’Occitane’s share) at €3.6bn, suggesting a low implied valuation of €1.5bn for L’Occitane ex-SDJ based on Group’s total valuation of €5.1bn now - considering ex-SDJ’s expected EBIT of ~€200mn in 2024E (or 7-8x forward EBIT multiple)

New channel boost: SDJ has quickly risen to be the no.1 brand in “body lotion”, “perfume mist” and “body wash” categories on ulta.com, just 3 months of entry into the channel. Coupled with positive feedback from channel check, this suggests that the brand will likely have a favorable prospect of penetrating further into the Ulta, a channel that generates even more revenue than Sephora U.S. (in 2022), fueling a new phase of growth and propelling the brand’s revenue beyond market forecasts

Longevity of the SDJ brand: predicting the enduring success of a young brand like SDJ is challenging, yet early signs incline me towards a positive outlook: 1) SDJ has found a target audience (Gen-Z consumers in Western countries who embrace the ethos of self-love and self-joy) whose needs are very well addressed by its brand messages and offerings; 2) it has a founder/ brand steward who has a keen sense of running and enriching a beauty brand; 3) it has demonstrated the knack of quickly iterating and launching new best-sellers, and even carving out new product niches (body cream, perfume mist…)

Capital allocation: my analysis suggests that the company's track record on M&A might be better than market perceives, with a 75% “success rate”, achieving 36% return on invested capital for SDJ and ~5% for Elemis in 2023

Shareholder returns: dividend payout ratio had been increasing and reached 40% in recent years (2021-2022), driving a ~2% yield; more impressive is that the company’s efforts to maintain the payout ratio during years when operational results are under duress

History of L’Occitane

L’Occitane was founded in 1976 by Olivier Baussan, with the purpose of creating a company that celebrates and preserves the traditions of his native Provence. L’Occitane en Provence develops and produces most of its products in France, with a focus on natural ingredients. The brand’s growth has been driven by retail expansion, running 1,362 self-operated stores by 2022.

In recent years, the company has stepped up acquisitions of other brands when it saw the growth of the main brand slowed. The company acquired Elemis in 2019, a high-end British skincare brand focusing on anti-aging facial treatment, and Sol de Janeiro in 2021, a U.S. body care and fragrance brand inspired by Brazilian culture - The latter has become the main driver of Group’s growth. Group leadership’s philosophy of managing the acquired brands is giving each as much autonomy as possible, to drive entrepreneurship and creativity.

Sol de Janeiro - SDJ (13% of revenue in 2022)

I start with the brand that accounts for only 13% of Group revenue in 2022, because I believe it is THE key to our investment thesis, and the main driver of Group financials for the next few years. I project the brand to surpass L’Occitane en Provence’s revenue in 2025 and EBIT in 2024, while the market has not given it enough respect in valuation potentially due to its currently smaller size (1/5 of L’Occitane en Provence’s revenue in 2022)

The market: the global beauty and personal care market was valued at US$536bn in 2022, within which skincare (US$152bn) and fragrance ($58bn) were the most relevant subsegments for SDJ. In the U.S., beauty brands sell through specialty chains (Sephora, Ulta…), general retail outlets (Walmart, Target, CVS…), or own stores (L’Occitane, Bath & Body Works…). SDJ went for the first route, and has become one of best-selling brands on Sephora, contributing ~10% of Sephora U.S. revenue in 2023

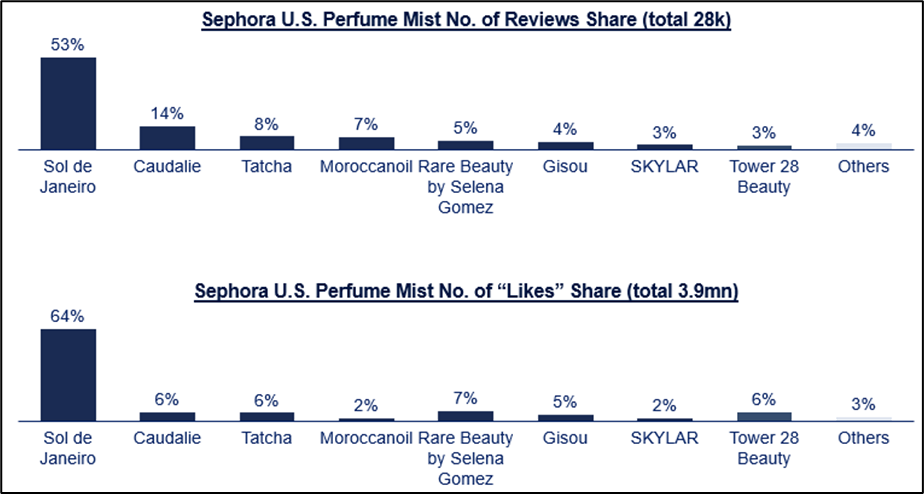

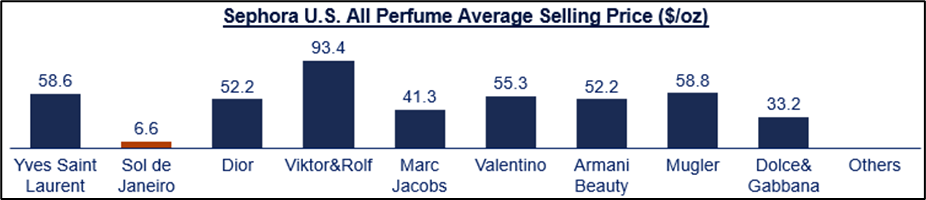

Sephora success: I conducted a primary data scraping on sephora.com to verify SDJ’s success at the channel – SDJ has become the no.1 brand in both body lotion and perfume mist categories on the platform, contributing 45% of total reviews and 51% of total “likes” in body lotion, and 53% total reviews and 64% total “likes” in perfume mist. The brand’s SKUs also rank very high on “likes/ reviews” ratio – which I feel is an indication of “relative consumer interests” – having 5 of the top 7 in body lotion and 7 of the top 7 in perfume mist. If I extend the scope of perfume mist to include all perfume, competition can become more intense, but SDJ is still a top 2 reviewed brand and the top 1 “liked” brand, with a clear distinction in target audience – all other major brands play in the premium+ category, with unit price on average 6-7x more expensive than SDJ’, leaving SDJ the only major player in the affordable segment (see appendix for detailed summary of primary data scraping results for sephora.com)

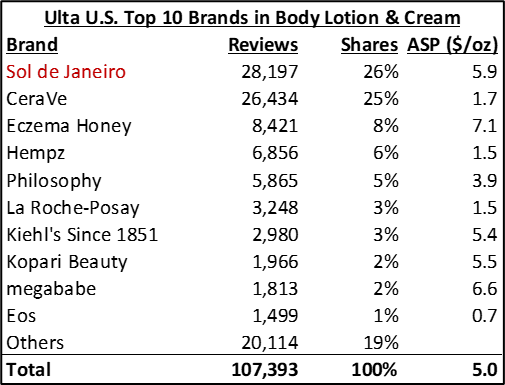

Ulta opportunity: SDJ expanded its retail presence in early 2024 by entering 700 Ulta stores (total 1,374 Ulta stores in the U.S.), after its previous exclusive deal with Sephora ended. Market remains uncertain about SDJ’s performance potential in Ulta, yet our research revealed positive signs: (1) primary data scraping on ulta.com shows that just 3 months after entering the channel, SDJ has already become the no.1 reviewed brand in body wash (for which it ranked no.3 on sephora.com U.S.), body lotion, and perfume mist (see appendix for detailed summary of primary data scraping results for ulta.com); (2) our channel check revealed positive feedback about SDJ’s sales so far in Ulta, suggesting potential for further expansion into more of Ulta’s ~1.4k stores; (3) risk of cannibalization with Sephora appears low as most Ulta stores are generally situated in less premium and more remote locations vs. Sephora’s, and the two channels cater to different consumer groups

Global expansion: SDJ kicked off global expansion in late 2023 focusing first on Europe and Australia, whose consumer preferences are more similar to those in the U.S., and the initial feedback has been positive. However, I feel expansion to APAC, especially eastern Asian countries like China and Japan, can be more challenging – the local consumer preferences for skin whitening (vs. tanning) and lighter cream textures, and a shyer and less attention-seeking culture are not a direct match to SDJ’s outgoing brand ethos – and thus the brand may need to tweak its product or message for a more successful entry. On the other hand, consumers in SEA countries have shown more inclination towards self-affirmation and self-joy, and can be an easier audience for SDJ to convince. I modeled a very cautious store expansion in APAC for SDJ

The founder: I feel Heela Yang, who still owns 17% of the brand, is a proficient brand steward. From several of her online video interviews, I noticed that she is an attentive listener, is quick to adapt, and thinks unconventionally – she went against “market wisdom” in terms of product naming and color theme choosing, and her decisions have proven to be effective. I like her approach of running the brand – different from most other skincare companies that center around solving a particular skin problem with some particular ingredients, she started with the brand manifesto: the self-loving and self-confidence message from the Brazilian culture that she wanted spread; she then decided on the product categories, ingredients, coloring, and packaging based on the central message. I feel such approach can increase the brand’s enduring relevance as it centers on a positive message that has long lasting value, rather than a product functionality that can more easily go out of trend

Sustainability of SDJ’s success: predicting the enduring success of a young brand like SDJ is challenging, yet early signs incline us towards a positive outlook: (1) a key element of a long-lasting brand is to be able to find a clear target audience that really resonates with its offerings – SDJ certainly has found its own in the younger generation in Western countries who embrace self-love and self-joy; (2) the company has a knack of quickly iterating and launching new best-sellers, and even carving out new product niches – notably recreating the body cream and perfume mist categories; (3) the brand’s previous flagship products, such as the Bum Bum cream, continue to perform well and drive brand growth 5+ years after launch, showcasing its offerings’ long shelf life; (4) buyer retention rate is 40-50% at Sephora (according to CICC analyst) and 30% at brand.com (according to company IR); the 40-50% retention rate at Sephora is considered top tier

Beating the expectation: current market expectation for SDJ’s 2024 (FY25) revenue yoy is 40~60% (according to Daiwa and CICC analysts). By assessing its channel penetration and per store sales improvement opportunities, I feel it will be hard for SDJ to not exceed the expectation. I value the brand at €3.6bn for L’Occitane’s portion (based on 75%/ 35% revenue growth in 2024/ 2025, 24% EBIT margin, 24% tax rate, and 13x multiple, discounted to today at 7% WACC) – this suggests that either the implied valuation of L’Occitane ex-SDJ (€1.5bn) is quite low (based on €0.2bn EBIT in 2024E), or that the market is undervaluing SDJ against its intrinsic value (if my projection is not off). I believe such disparity and mismatch give us a good buying opportunity

L’Occitane en Provence (67% of Group revenue in 2022)

I didn’t devote too much research time into L’Occitane en Provence in this research, despite it accounting for 67% of the Group’s revenue in 2022, because my investment thesis does not hinge on the specific performance or success of this brand. I believe the investment rationale can still stand with conservative assumptions about L’Occitane en Provence, provided it maintains its revenue size with relatively stable profitability for the next few years.

Retail network: I feel that the size of L’Occitane en Provence’s retail network, one of the major drivers of its revenue, has reached a relatively “optimal” level – meaning not much room for further growth. The company rationalized the number of its owned stores by 15% in 2019-2022, closing down unprofitable ones in regions like North America and Europe. Looking ahead, the company guided a plan to open 15-20 new stores in China, but also to close several more stores in Europe – I think the company’s priority now is to stabilise its retail network and focus on per store sales and profitability. I do applaud such strategic direction though, because “stretched” expansion can generate terrible return on investment

Buyer persona: buyers of L’Occitane en Provence are not those who look at absolute performance of the products, but those who seek quality products (but more on the balance side) that can offer them a good “spa-like” experience with enjoyable scents – mainly middle class or high incomers who buy the products to make themselves “feel happy” and unwind from daily stress, or to give others as gifts. A “benefit” of such value proposition is that the brand does not require high R&D investment (avg. 1.1% in 2020-2022), but it does need to spend on distribution (avg. 43% in 2020-2022) and marketing (avg 14.1% in 2020-2022) to maintain customer attraction. I expect the marketing ratio to continue to be high – the company also acknowledged that high spend is required to stay relevant in an increasingly competitive skincare market

Sustainability: despite no plans for expanding its retail network, the brand remains sustainable due to several factors: (1) it has been in operation since 1976; during 2019-2022, when it closed down 15% of its self-operated stores (and 25% of its wholesale locations), its revenue still increased by 10% thanks to higher per store sales; (2) the brand has shown ability to be flexible in adapting for market trends and local customer preference, which can contribute to sustained relevance; (3) over the years, it has developed some highly popular and long-lasting SKUs (shea butter hand cream, Immortelle serum/ youth oil, almond shower oil…), driving recurrent purchases; (4) it has built a long track-record of strong emphasis on sustainability elements (natural ingredients, ethical sourcing…), a commitment that has been acknowledged by customers

Elemis and Other Brands (Elemis 12% of revenue, Other brands 9%)

I spent even less time on Elemis and other brands due to their even less impact on the investment case, although I do feel some of them have good potential. Due to lack of visibility of their future development, I took a cautious approach in my forecast

Elemis: British skincare brand focusing on high-end natural facial cleansing and skin wellness, with products sold in retail and specialty channels (such as spa lounges and cruise ships). I didn’t bake in high expectation for this brand – 5.8% revenue CAGR for 2022-2027 (vs. 16% in 2019-2022) and 17-20% EBIT margin for 2022-2027 (vs. avg. 22.4% in 2019-2022) – due to lack of visibility on its future growth potential and assessment that competition in anti-aging skincare sector will be fierce. In addition, I feel the relatively frequent discounting in the past few years may devalue its brand equity

Other brands: Erborian (Korean brand with a focus on natural herbs) and L’Occitane au Brésil (L’Occitane localized for the Brazil market) have been profitable and consistently performing well over the years (including post-Covid), but are still small in size. Melvita (French brand focusing on natural ingredients) has faced some recent struggles (revenue decrease, operating losses) since 2019, incurring €22.8mn impairment of goodwill in 2022 (45% of its total GW), but the Group is still remaining hopeful for its turnaround. LimeLife (U.S. brand employing the social-selling model) delivered bad performance after Covid (revenue down, huge operating losses), incurring €53mn impairment of goodwill in 2022 (>50% of its total GW); it was given a mid-2024 deadline to turn around but I have yet to seen any material improvement – I forecasted Group to sell the brand before 2025

Management and Corporate Culture

Bottom-up approach: Group leadership’s brand managing philosophy is to give individual brands as much freedom and autonomy as possible in running their operations, aiming to bring out the most entrepreneurship and creativity in each brand. One drawback of such approach is the insufficient integration and synergy across the group, resulting in missed opportunities of efficiency gains

Family involvement: there is still heavy involvement of the Geiger family in L’Occitane’s business – Adrian Geiger, chairman’s younger son, is in charge of L'Occitane en Provence; Nicolas Geiger, the older son, is in charge of L’Occitane au Brésil and coordination among brands

New CEO: Group appointed new CEO Laurent Marteau in Jan 2024, replacing André J. Hoffmann, Vice Chairman and ex-CEO of the Group; an industry expert pointed out that one key task for the new CEO is to “manage the family”, which could significantly influence his ability to lead the company successfully

Sustainability (ESG): the Group has been consistently promoting ESG since inception, emphasizing the use of natural ingredients across all its brands; it has earned a reputation and trust among modern consumers as a sustainable beauty brand, something that is not easy to achieve and takes track record as consumers nowadays become increasingly informed and discerning

In the next session, I’ll share my analysis of the company's financials and valuations, and will cover:

My projections for the company’s topline and bottom line growth, by brand

Analysis of capital allocation and M&A effectiveness

Valuation analysis

Additional supporting charts and diagrams